The hottest story coming from Iceland now is the one about the government-initiated debt relief to households. Here is my take on it, focused only on handful of all the questions and issues related to the act itself and, perhaps more importantly, the potential economic development in the future. Especially on that front we have a sea of unanswered questions. Is this going to be inflationary? What about economic growth, unemployment, investment levels, etc.? The balance of payments? Will this help or hinder the abolishment of capital controls?

First some useful links (in English) that I found. They are unfortunately not many... classic Icelandic lack of communication problem... (if you've got some others, please leave a comment):

FAQ on the website of the Prime Minister's Office

The news itself on the same website

Bloomberg -

Creditors in Iceland Banks Face Pressure to Speed Up Settlement (by an Icelandic journalist).

The basics

Framsóknarflokkurinn (e. The Progressive Party, PP - they are conservative) promised to carry out a debt jubilee if it would be elected into power in the last general elections. They were. The other half of the coalition is Sjálfstæðisflokkurinn (e. The Independence Party, IP - conservative).

Those two parties did not agree on how the debt should be cancelled. The PP wanted to straightforward cancel it. They were talking about up to ISK 300 billion just before the elections, the actual amount turned out to be half that. The IP thought that cancellation would be impossible since it would either be simply illegal on the grounds of property rights and / or too expensive for the State in case the State was going to foot the bill for cancelling the debt of households. Their take was to use the tax system and create incentives for people to use the 3rd pillar of the pension system - the private pension holdings - to get tax-free additional income to be spent on paying down debt and only to pay down debt.

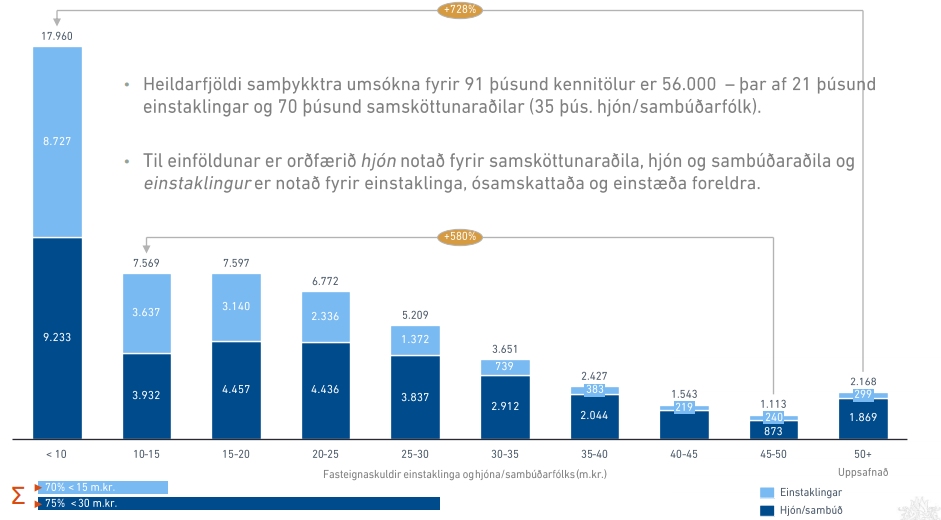

The outcome is a mix of both. ISK 80bn. (roughly GBP 400 million) of household debt will be outright cancelled. Additional ISK 70bn. are to become available via allowing people to use their 3rd pillar pension savings in the next three years, to pay down their household debts.

So what's the crack?

Icelandic households will get ISK 150bn. (GBP 750 million) of their household "cancelled", spread over a four year period. I say "cancelled" because they are in fact paying down ISK 70bn. of it themselves, the only thing is that they get to use tax-free pension savings to pay down that part. And that makes perfect sense by the way: why save in an illiquid form at 2-3% real interest when you have debt to pay that charges a 4-5% rate of interest.

The rest, ISK 80bn., will be outright cancelled in four annual instalments although the borrower will feel the positive impact on his monthly payment burden immediately. Each household that has an indexed mortgage, partially or wholly, (

check this link to see how indexation of Icelandic mortgages works), specifically declared to buy a property for own use (

buy-to-let mortgages are excluded!) will get a maximum of ISK 4 million of the debt written off. Non-indexed loans get no write-off but the tax-free pension savings can be used to pay additionally onto the principal in the future. The tax-free pension savings can also be saved and later used to buy a flat. This is why they say that even current tenants will benefit from the measures. If the household got its debt cancelled via e.g. the 110% measure this will be accounted for and the current write-off will consequently decrease.

The following is a copy-paste from the slides about the measures. The way you should read this is the following. The x-axis is the time when an ISK 15 million mortgage was taken out. The graph (grey area) shows the nominal amount of that debt today (Remember, the principal of indexed Icelandic loans INCREASES in value parallel with the CPI. That's the reason why an ISK 15 million mortgage taken out in e.g. September 2001 would amount to about ISK 25 million today according to the graph). The blue area is the debt after the debt has been cancelled and the light brown (beige??) area is the amount of the mortgage once a 3 year private pension pay-down has been accounted for. So the decrease is read vertically and depends on when the loan was taken out. Click to enlarge.

The principal of an ISK 15 million mortgage and how it is affected by the jubilee, depending on when it is originally taken out

Now, most of the questions, and some answers, about how and why and what for and all that can be found in the FAQs from the Prime Minister's Office. So head over there to read further on how the whole thing is carried out. I would rather spend time on some other issues, such as:

Is this significant?

That depends on how you look at it I suppose. This jubilee is not gigantic in comparison to the debt that has already been cancelled since 2008. On that note, I honestly think this nice info-graphic, which is circulating on Facebook from a group that is politically, well, not keen on the current government, says it all. To give the current government some rightful credit (pun intended): their measures are more significant, by a mile, than the previous government's measures (because they had nothing to do with the pink part of the left column).

Comparison of how much household debt has been cancelled in Iceland since The Crash.

The headline ("heimsmetið") is a reference to the prime minister who said that his government's jubilee was a "world record". The left column is debt that was cancelled during the coalition rule of last government. The colours represent the following: purple (12bn) - special interest benefits, pink (155bn) - correction due to illegal FX-indexed loans (this came through the justice system and had nothing to do with the former government), orange (8bn) - special debt measures, yellow (48bn) - the 110% way (any debt above 110% of your property value was written off), grey (15bn) - increased interest benefits, blue (70bn., the IP's campaign colour) - Tax-free pension savings, green (80bn., the PP's campaign colour) - debt jubilee.

So in comparison to the previous write-off of debt in Iceland, governmentally initiated or not, the current jubilee is not so huge.

However, it is significant from the point of view of proving that this is politically possible! And that's something for other nations to learn from! Jubilees do not need to be a thing of biblical times! (But of course, that does not mean that they are always a smart move!)

But how are they paying for all this?

Right, that's a bit hazy to be honest. The short answer on the list of FAQs on the website of the prime minister's office is a classic nonsense answer that doesn't add any value:

"How is the debt relief financed? The Treasury will collect increased revenues in the next four years to cover the cost of additional state expenditure resulting from these actions. The actions will therefore neither be financed by additional Treasury borrowing nor with the granting of state guarantees."

Right, so the no-bullshit answer is that you're going to increase taxes - or "collect increased revenues..." Then just say it!

Where are they going to "collect increased revenues"? From the old banks. Through taxation. Specifically, they are going to tax the estates of the old banks, i.e. the bankrupt banks since 2008. Their liquidation process is going veeeery slowly, to a large extent because of the capital controls and the tug of war between them and the liquidation process of the old banks: the capital controls hold it back but the estates have to be liquidated in the end before we can abolish the capital controls. Well, that's a nice one: like being a driver with two back seat drivers, one demanding you drive faster and the other demanding that you slow down. Which one are you going to make unhappy?

The government is going to make the old banks unhappy. Besides outright taxation on the them to pay for a debt jubilee for households, they are considering changing laws that would force them to speed up the liquidation process.

I've got two immediate concerns about this.

First, those are two birds in the bush but not one in the hand. Are we definitely sure that they can tax the old banks? This sentence alone from the

slides says it all (slide 56): "

The committee [behind the debt jubilee] assumes that the measures will be fully funded over a period of four years" (i. "hópurinn gefur sér þá forsendu að aðgerðin verði fullfjármögnuð á fjórum árum.").

Great going guys, I do this all the time as well! I always just book my vacation to French Polynesia and just assume that I can finance it! ISK 80 billion!? Pennies mate, I'll pick them up off the floor one day!

And even if they can tax the old banks specifically (there are some concerns about whether it would be constitutionally possible or not), won't the old banks, which are the main owners of Arion and Islandsbanki, not just pass at least part of the cost onto their customers? Competition in the banking industry in Iceland isn't great you know.

Second: OK, if we can tax the old banks to get cash for a debt jubilee, couldn't we have used the money for something else? Like not practically shutting down the Icelandic public radio? Or pay decent wages to doctors, nurses etc.? Not putting myself up against the debt relief as a principle, just pointing out that we didn't have to spend all the cash on it.

Or maybe we can tax them even more and spend that tax income on something nice!?

But how do they actually do this?

1. The mortgages are split up into "primary" and "secondary" parts.

2. The primary part (about 87% of the mortgage to be written down) is the new debt of the borrower. This loan has the same loan stipulates as the original loan, i.e. same rate of interest, indexed to CPI, etc.

3. The secondary part is interest and indexation free.

There are no payments of that debt. Both of the loans are on the balance sheet of the borrower and the financial institution that owns the original loan. The total payment burden therefore contracts immediately and not over four years.

5. Annually, the State buys back 25% of the original amount of the secondary loan from the financial institution (hence the fact that this will take four years to finish). This is roughly ISK 20 billion annually, hence the total ISK 80 billion write off. The debt is then written off. The income to fund this is meant to come from the estates of the old banks themselves.

What about the economy?

The government estimates that with all this they will manage to get household debt below 100% of GDP. Such a debt level is still quite high and may still be a barrier to economic growth and financial stability, especially since interest levels in Iceland are stupefyingly high in comparison to other economies.

Nevertheless, this should help. Analytica, a consulting company back home, reckons the effects of the jubilee will be the following for 2014 only:

- economic growth: +0.1%

- inflation: +0.1%

- current account balance: -0.2%

- consumption: +0.4%

- investment in new properties: +2.0%

My take in short

Now, there are some good things about this measure.

First of all, they did it! Jubilee is here, well done guys! You proved this is politically possible and economically this does not seem to be an absolute nonsense. So this opens up the possibility of doing this in other countries. Whether that would make economic sense has to be discussed for each economy. Some very indebted households will feel quite relieved and this will have positive impact on the economy although the impact may be short lived (see more why below). The tax-free pension part of it all also makes perfect sense and simply boils down to the fact that it is not smart to save on 2-3% rate of interest when you owe debt bearing 4-5% rate of interest.

But I do have to admit that I have concerns, besides the obvious ones like the taxation issue (which may well enough not be so important). There are a few reasons why.

First, the primary loan, or the new loan, that the borrower has to pay off will still be indexed, just like the original loan that now is being partially written off. We will therefore still have all the negative effects of indexing mortgages in Iceland, including more volatile inflation, higher inflation, higher rate of interest, lesser effectiveness of the monetary policy and the risk of having to have another debt jubilee in 10 years time or so.

Second, and closely related to my first concern: although there is no

direct increment in money supply because of the measures we can, I believe safely, assume that not only will we have some potential demand-pulled inflation immediately in the wake of all the jubilee but increased credit demand as well (especially if we have an increase in moral hazard due to all this: will people take on more debt because they anticipate another debt jubilee in the future?). As the increased credit demand will be met with new loans that increase the money supply we will end up with further inflation pressures. And because the principal of indexed debts will grow with more inflation we will get some, or even all, of the "jubileed" debt back. The Central Bank will also respond with an interest hike to try to hold credit demand back. That will hit the borrowers with non-indexed loans as their interest rates are potentially readjusted upwards. (More effective and sensible way of limiting credit growth and inflation would be to impose direct credit controls and connect them to the banks' own net holdings of liquidity in foreign currencies. But I doubt the Central Bank will go down that road: you can't teach old dogs how to sit).

Why, oh, why did they not make it compulsory to change the new primary loan into a normal non-indexed loan? A golden opportunity to get rid of this pest that indexed mortgages are has been wasted!

Third, although the net assets of the old bankrupt banks will contract (assuming everything goes according to plan) we will still have "considerable" pressure on the balance of payments because of increased consumption and demand. Now, of course, part of the reason for those measures is to revive household consumption. But if we will get into even further riskier waters with the balance of payments than we are in, doesn't that just signal that the exchange rate is too strong? And imagine what will happen when and if the exchange rate goes down: inflation goes up, principal of debt grows back, we're back on square one.

So again: why, oh, why did they not abolish indexation parallel to those measures?!

Fourth, and this is perhaps my most serious concern.

We haven't fixed the institutional drawbacks of the Icelandic economy. Besides still having the indexation on mortgages, we still have a high self-imposed rate of interest stemming from the pension system. (It is regulatory required to get a real rate of return of 3.5% and it controls assets equal to about 120-130% of GDP. What do you think will happen to the long term rate of interest with such gigantic buyer of financial liabilities who demands a high minimum rate of interest. Has anybody heard of

monopsony?). We also still have high short-term rates, to a large extent because of the indexation.

So I fear that the net effects of this debt jubilee will not be significant in the long run. At least from an economic point of view. Politically, this may fuel some fires, even in other countries where over-indebted populations may be nudged to demand jubilee there as well. In some cases those potential jubilees might make sense. The taboo of debt relief has just been delivered a blow. Maybe we can actually discuss it in a more sensible manner from now on and not with cries coming from both sides.

That is all well and square, but when it comes to the Icelandic economy, I fear we will only have short spurts of economic bounce back. It is not enough to cut the leaves of the weed, we need to dig out the roots as well.